As the American economy matures in an economically competitive world, Nominal and Real Economic Growth Rates have gradually decreased. It is often called the "New Normal." Several features are represented in this "New Normal." Business cycles are longer but with slower growth. And except for the Great Recession, in the main triggered by a failure to judiciously regulate the real estate and derivatives market, recessions are more shallow and shorter. With that said, here is this week's contribution to the debate.

Economic Development in the US: Looking Back 35 Years

America has experienced a Nominal (nominal means considering inflation) economic growth rate of 5.4%, on average. This also equates to an average of $9.5 billion in national output each year since 1980. While these numbers may sound good to the average citizen, Real economic growth (growth adjusted for the rate of inflation) has been closer to 2.4% annually with real output of $3.7 billion each year.

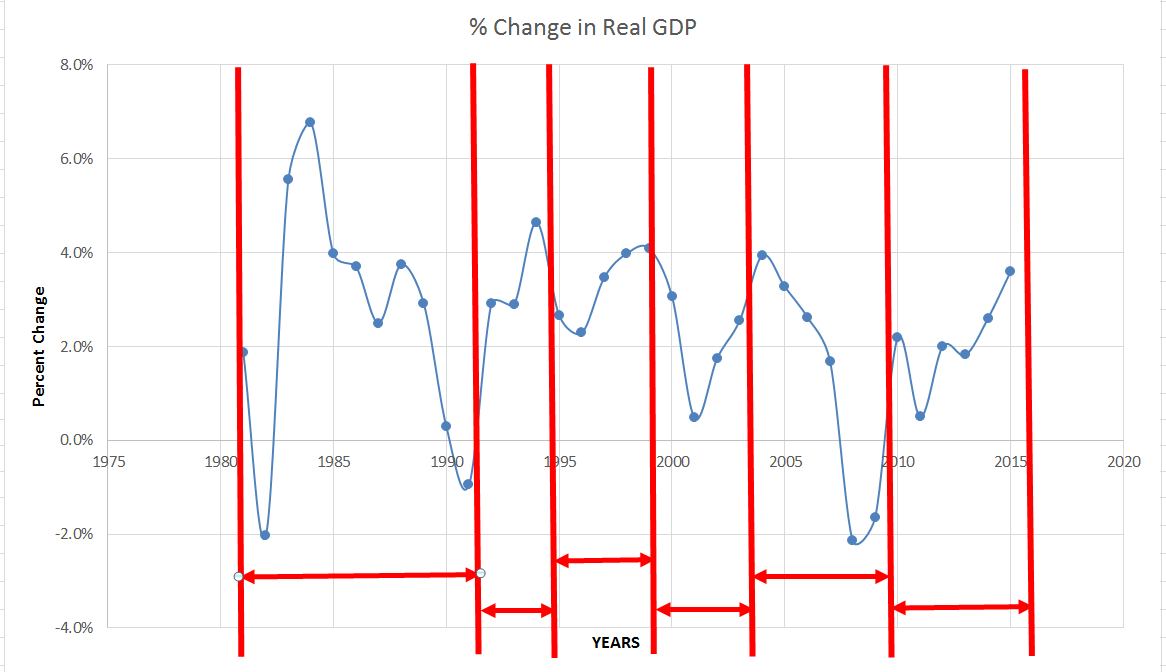

Recently, though, Americans have seen Real growth rates of 4% in 2015. This number is an improvement over the historical average. To arrive at these figures, economists look at business cycles – recessions and expansions – to analyze and compare economic growth (see Graph 1).

Graph 1

Governments seeks to limit recessions and spur and prolong economic expansion. Various American presidential administrations have introduced initiatives and policies to improve the economy. Recent action such as the American Recovery and Reinvestment Act or “Economic Stimulus Package” of 2009, was introduced in the wake of the 2008 collapse of the real estate market.

In reviewing the actions of various administrations over the past 35 years (Chart 1), business cycles appear to be getting longer. For example, the Reagan administration had a two year peak to trough cycle. The Obama administration, by contrast, has produced economic growth for most of his presidential term. So let’s take a deeper look at the Real growth rate over the past 35 years. And let’s also look at some specific period(s) of time in the last 35 years.

Chart 1

US Presidents over the past 35 Years

|

Growth Rates (within Presidential Term)

| |

Highest

|

Lowest

| |

Reagan

|

6.8%

|

-2.0%

|

Clinton

|

4.7%

|

2.3%

|

GW Bush

|

3.9%

|

-2.1%

|

Obama

|

3.6%

|

-1.6%

|

HW Bush

|

2.9%

|

-0.9%

|

Presidents are all faced with different economic challenges and outside events that have great impact on economic growth. George W. Bush ended his eight-year term with the real estate market collapse in 2008 and Obama inherited that same economic mess. Reagan saw both high and low rates of growth, while Clinton came into office during a great expansion in computer technology followed by the dot.com boom and bust.

From some high rates of growth in the 1980s, rates of fluctuation in economic growth have flattened and declined somewhat over this period of time. And until the collapse of the real estate market in 2008, the economy has steered clear of major recessions and major declines in growth. Overall, in this past 35 year period there have been six business cycles. These are shown, with their peaks and troughs, in Graph 1.

If we look at the secular trend over our period of time, Real growth rates have slowed in volatility. This is in large part impacted by automatic stabilizers like the welfare system, unemployment insurance and the personal income tax system. Automatic stabilizers counterbalance instabilities in the economy activity without direct involvement by policymakers. In 2000, a study done by Alan Auerbach and Daniel Feenberg published in their article “The Significance of Federal Taxes as Automatic Stabilizers" in the Journal of Economic Perspectives, assessed that reduced income and payroll tax balances about 8% of any GDP decline. Unemployment insurance payouts further stabilizes GDP. Estimates indicate that unemployment payouts are 8 times more effective per dollar in economic stimulus relative to the same amount being saved rather than being put in circulation

Economic growth and contraction were also affected by Federal Reserve Board policies during this period of time. In 1979 incoming Federal Reserve Board Chairman Paul Volcker faced an economy with runaway inflation which peaked in March of 1980 at 14.8%. Contractionary monetary policy was put in place to cool inflation. Fed Fund rates were raised to 21.5%. These actions by natural result triggered a short, very deep recession in 1981-1982 with unemployment over 10%. But when the economy came out of this recession, inflation stabilized and a more stable economy that followed historical business cycle emerged.

Another economic trend emerged during this 35-year period, increasing trade deficits. From 1980 to 1991, trade deficits remained benign. But in 1997 trade deficits rose steeply, peaking in 2006, but never returning to their previous levels.

These trade deficits are in effect placing a claim against future economic output to maintain current output. Eventually, the interest paid on this debt will overtake America’s ability to maintain this pattern of borrowing.

These trends are not sustainable. Employing regression analysis upon the current account deficits and foreign borrowing demonstrates this. In simple terms, the US is living beyond its means.

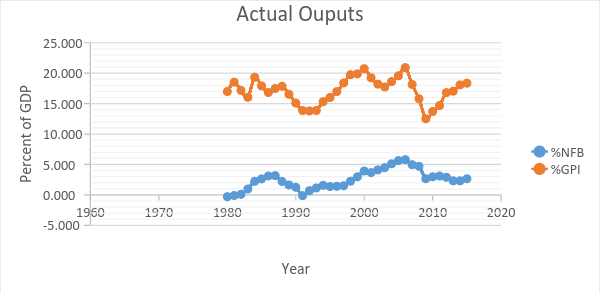

If we examine these trends by comparing Net Foreign Borrowing (NFB) with Gross Private Investment (GPI), we see that NFP exceeds GPI by roughly 15% over our 35 year period as seen in Graph 2.

Graph 2

Written by Alison Blodgett, Eric Hoover, Jeffrey Wilder and Julie Feightner.

Added by Rob Feightner: Blathering about "brangin' the jawbs bak," protectionist trade policies and hog trough tax policies that lower the marginal rate for rich LLC owners to an amount lower than their highly compensated employees will increase the deficit to records only Arthur Laffler could love. This deficit and the exploding debt may well knock US treasuries off their spot as the universal risk free rate of return. And raise the cost of borrowing in the US. But the Mezcuns will pay for it.

US manufacturing is operating at record levels. Manufacturing just needs fewer workers as automation and robots supplant humans. This trend is indefagatible and irreversible. Many fast food workers, one of the last industry hiring great amounts of unskilled labor, will be automated. And automation will hit healthcare with patient care robots. Not everyone can get a job selling health insurance across state lines, teaching in privatized schools, or marking up the price of Medicare vouchers.

Ironic isn't it, that just as the last few threads of the American safety net are being ripped down, labor dislocation on the scale of the Industrial Revolution lurks not afar on the darkling plain.

THE DESERT OF THE REAL IS BACK! NOT EVEN A WALL AND RUSSIAN COLLABORATORS CAN RESTRAIN IT.

No comments:

Post a Comment